Calls Answered 24/7

Calls Answered 24/7 e-Mail Us Now

e-Mail Us Now

If you’ve been injured in a car accident, one of the most important factors in your claim is the statute of limitations. That is the legal deadline for filing a lawsuit. Failing to file within this timeframe can result in losing your right to seek compensation.

So, for how long after a car accident can you claim for your injury? The statute of limitation varies from state to state. Depending on where you live, you likely have at least two years to file a claim. Some states give upwards of six years to sue for a car accident injury.

Understanding these deadlines can help you take the necessary steps to protect your rights.

Statute of Limitations by State

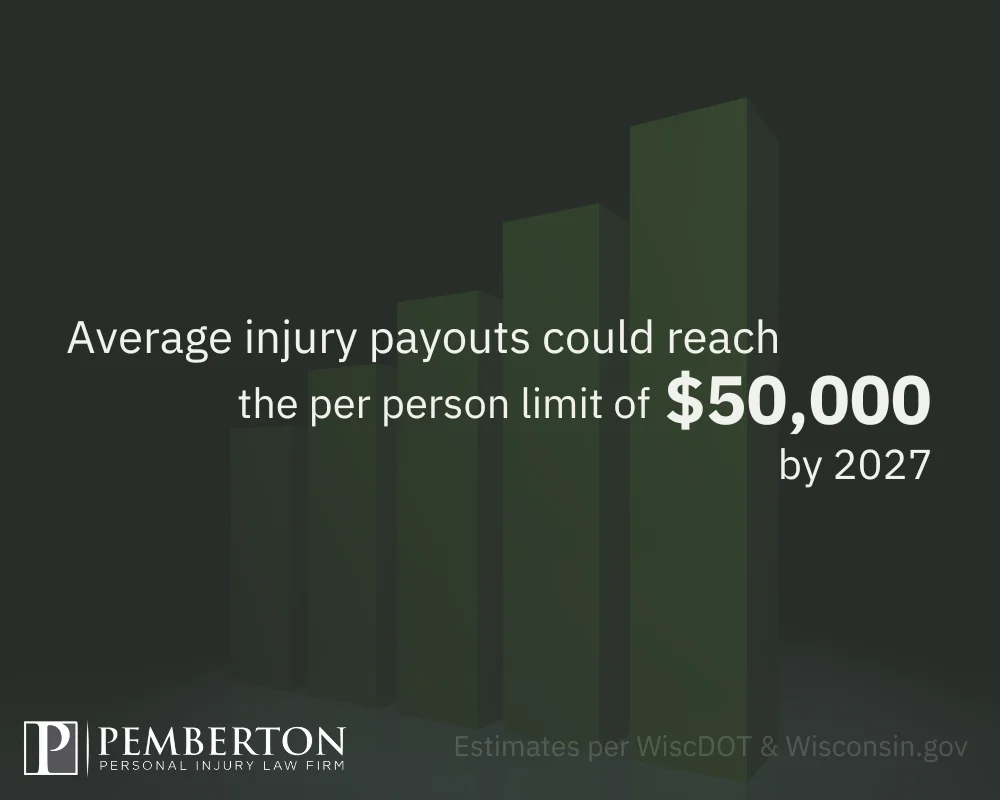

Wisconsin

In Wisconsin, the statute of limitations for filing a car accident injury lawsuit is three years from the date of the accident. In the case of a wrongful death claim, loved ones have only two years to file a car accident lawsuit. If you fail to file within this period, your claim will likely be dismissed (there are some rare exceptions).

Minnesota

Minnesota law allows victims of car accidents six years to file a personal injury claim. However, if the claim involves a wrongful death case, the statute of limitations is three years from the date of death, provided the death occurred within the six-year period following the accident.

Illinois

Illinois has a two-year statute of limitations for personal injury claims arising from car accidents. The clock starts running from the date of the accident. If a victim does not file within this timeframe, they will generally be barred from seeking compensation.

Other States’ Deadlines

- Iowa: Two years from the date of the accident.

- Michigan: Three years from the date of the accident.

- Indiana: Two years from the date of the accident.

- Missouri: Five years from the date of the accident.

- North Dakota: Six years from the date of the accident.

It is important to verify your state’s laws, as special circumstances can alter the filing deadline.

Why Do Statutes of Limitations Exist?

Statutes of limitations exist to ensure that legal claims are brought forward within a reasonable timeframe while evidence and witness testimony remain available and reliable. These deadlines also provide defendants with certainty that they will not face a lawsuit indefinitely.

Exceptions to the Statute of Limitations

While these deadlines are generally firm, there are some exceptions:

- Minors: In many states, the statute of limitations may not begin until an injured minor turns 18.

- Discovery Rule: Some states extend the filing deadline if an injury is not immediately apparent. In these situations, the statute of limitations might start when victims notice the injury instead of the accident date.

- Government Entities: If your claim is against a government entity, such as a city bus or state vehicle, you may face much shorter deadlines. Sometimes you have as little as six months to file a notice of claim in those cases.

How the Statute of Limitations Affects Your Claim

If you fail to file your claim within the applicable deadline, you lose your legal right to seek compensation through the court system. This means the at-fault party and their insurer have no legal obligation to compensate you.

Insurance companies are aware of these deadlines and may use delay tactics, hoping that you miss your opportunity to file.

Does Filing an Insurance Claim Extend the Deadline?

No. Filing an insurance claim does not extend the statute of limitations for a lawsuit. Many people believe that if they are negotiating with an insurance company, they can delay filing a legal claim. This is not true. If the negotiations do not result in a settlement and you miss the deadline to sue, you will lose your right to take legal action.

Steps to Take Before the Deadline Expires

To protect your right to compensation, take these steps as soon as possible:

- Seek medical attention: Obtain medical records documenting your injuries.

- Report the accident: Ensure the accident is reported to the police and, if applicable, to your insurance company.

- Gather evidence: Collect photographs, witness statements, and any other relevant documentation.

- Consult a legal professional: Attorneys can help you navigate deadlines and legal requirements. They can also ensure you file your claim on time.

Time Is of the Essence for Your Car Injury Compensation

Understanding the time limits for filing a car accident injury claim is vital. Missing the deadline could mean losing your right to your car injury compensation. Every state has different rules, so it’s important to act quickly.

Speaking with a personal injury attorney can help you understand your legal options, gather necessary evidence, and ensure your claim is filed on time. Taking action early can make a big difference in the outcome of your case.